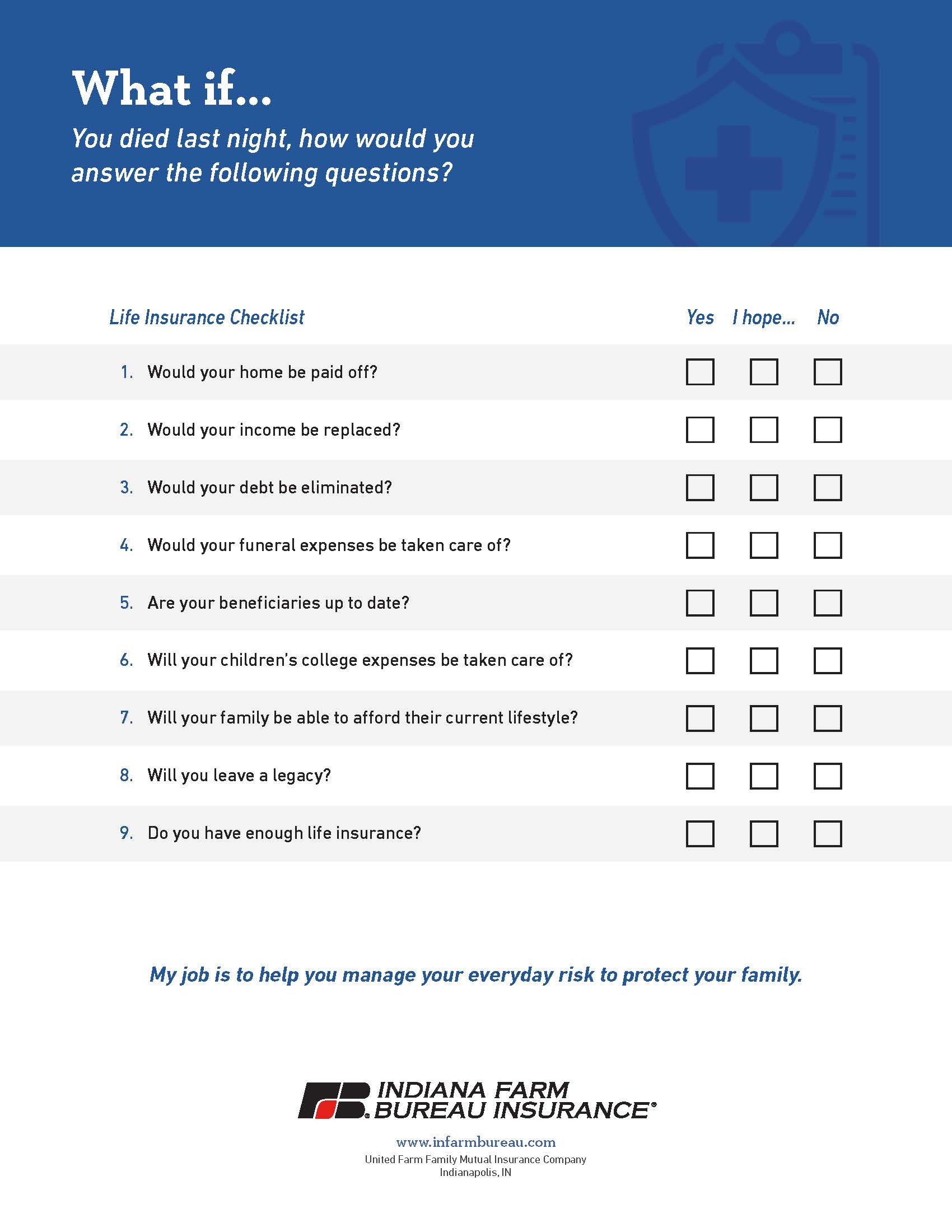

Picking the right benefit amount

Life insurance is love insurance

Let’s get it out of the way – life insurance is important, especially if you have loved ones who depend on you financially.

Like most insurance, life insurance is not something most people want to buy, and getting someone to admit that having some is important is a huge accomplishment. Acknowledging the need for life insurance is somewhat akin to admitting you’re going to die. And while everyone will at some point, no one truly wants to accept it.

But the questions surrounding life insurance can make the actual purchase feel intimidating.

* What kind should I get?

* If my employer provides it, why do I need to buy more?

* And the big one – how much should I get?

There is no wrong answer to the last one, except an answer that makes life insurance so expensive that it becomes economically unwieldy. A life insurance policy, or even a portfolio of different types of policies, should be tailored to meet financial needs and obligations.

A quick Google search for life insurance calculators can yield a multitude of results, many of which are tied to life insurance companies as lead generator tools. A very good one can be found at Life Happens, a not-for-profit organization created to promote awareness of life insurance. Its calculator tool is https://lifehappens.org/life-insurance-needs-calculator/.

The Life Happens calculator allows the user to determine how much income replacement is needed and for how many years, incorporates debts such as mortgages, loans, and credit cards, children’s educational expenses, and more. Users can then plug in how much life insurance is already owned, and the system creates a “need” report.

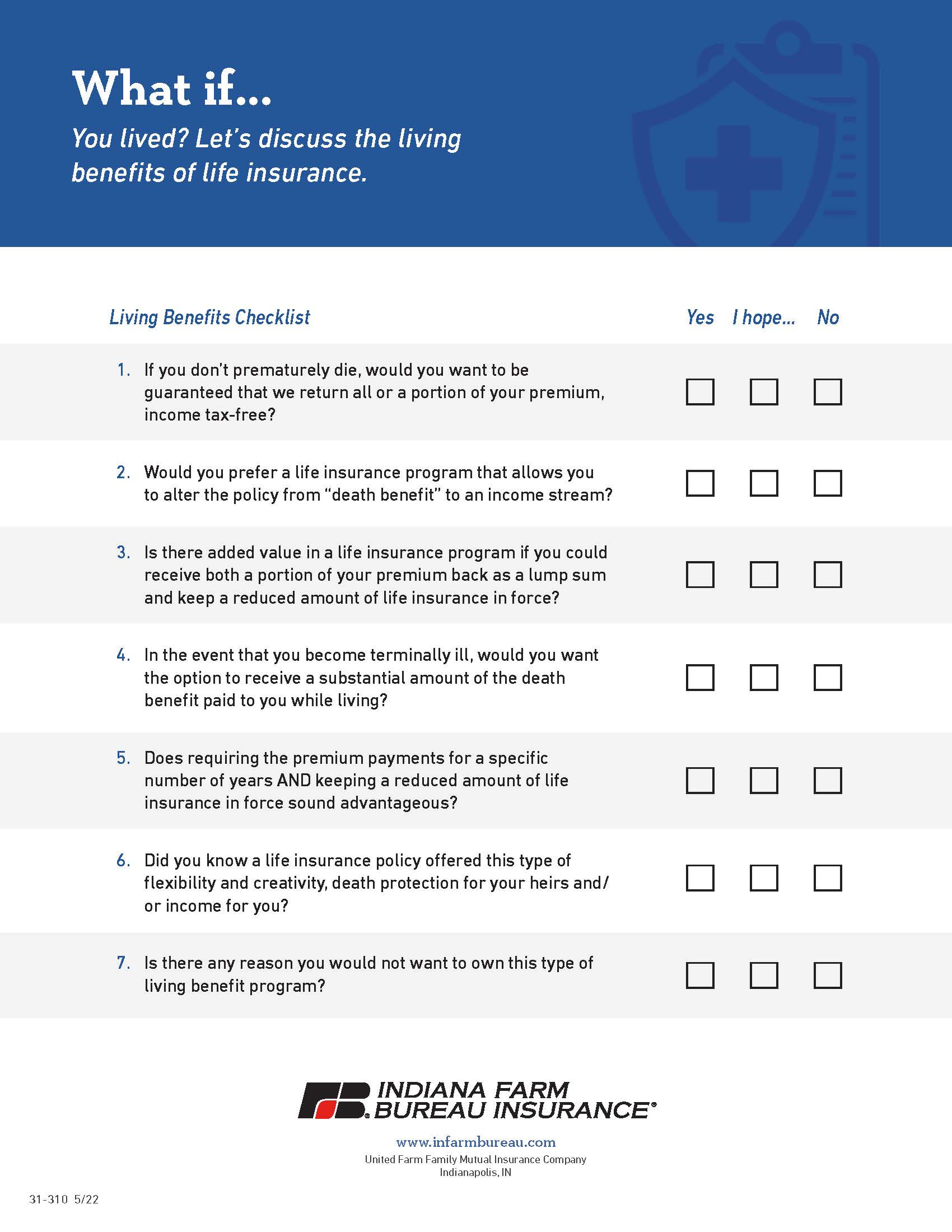

That life insurance need can be intimidating and create visions of exceptionally large premiums. It is then important to talk with a life insurance professional to understand how the needs can be met in the most cost-efficient manner possible.

Still, meeting all life insurance needs can exceed a reasonable budget. Consumers can then begin targeting the different parts of an overall need and create a life insurance program that hits one or more of them.

For example, if a mortgage can be paid off with life insurance proceeds, then the survivors might be able to use their income to handle other day-to-day needs. Or if life insurance can create a multi-year stream of income, then survivors can work that into a budget to pay bills and retain some degree of financial comfort.

Perhaps making sure children can go to higher education or advanced training is a priority. Life insurance benefits can be channeled into savings to meet those goals.

It is important to remember one truth – some life insurance is better than no life insurance, especially if you have people who depend upon you financially. Whatever end-of-life expenses that can be mitigated through life insurance are expenses that don’t weigh down survivors.

Life insurance is love insurance.

Alan T. Girton is a veteran agent with Indiana Farm Bureau Insurance. To learn more, visit https://www.infarmbureau.com/agents/Alan-Girton-Howard-Kokomo-IN.

| A guest post by

|