Updating your home and your insurance

Plumbing, electrical, roofing upgrades can save investment, lower rates

At a time when prices seem to be increasing across the board, it may be surprising how making updates to your home can lower your insurance premiums.

Many updates that homeowners should consider have to do with property protection and risk mitigation. But those are exactly the updates most home insurance companies want you to make to lower the chances that claims may be filed.

One of the first systems to consider for updating is the home’s electrical system. This system will include not only the breaker box, but also wiring and outlets throughout a home. In the simplest sense, the newer the system, the lower a home insurance premium will be.

Many standard line home insurers will not provide coverage on homes with outdated electrical systems, including knob-and-tube prevalent in many homes built before the 1940s. Some insurers will also reject applications where the home has fuse-based electrical

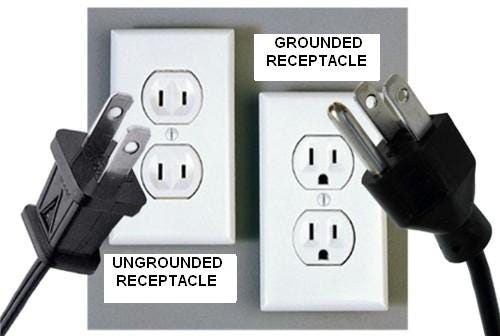

systems or not been upgraded above 100-amp service.

Homeowners should also be wary of systems that appear to have proper outlet grounding but actually do not. To check, a homeowner can take the cover off a three-prong outlet and pull the outlet assembly out. An up-to-date, safe system will have a third wire attached to grounding posts. If there is no third wire, it is possible the system may not have been updated.

Updating a home’s electrical system may seem costly, but beyond lowering home insurance premiums, doing it can reduce the risk of an electrical fire and loss due to power surges. It is strongly recommended to use an insured electrician to exam a home’s wiring system and replace or update it if needed.

Another key improvement homeowners can make to protect their investment and potentially lower home insurance premiums is replace the roof.

As traditional roofs age, the components in the shingle can degrade. Granules that make up the surface of a shingle can come loose, thus reducing the shingle’s ability to protect the underlying decking material. Aging shingles can also curl or crack, allowing moisture to get under the shingle and permeate the roof deck, weakening it.

A weakened roof deck may make it easier for protective shingles to come loose in high winds or even have the decking itself fly off, opening the home to damage from above.

Some home insurance companies offer discounts for installing new roofs, while others will remove ratings associated with older roofs. Shingle or metal roofs that have components listed with United Laboratories may even qualify the home insurance policy with additional discounts. Home insurance policy holders should consult with their agents to see if their roofs qualify.

One last improvement that homeowners can make to potentially reduce home insurance premiums involves updating a home’s plumbing system.

Older homes may have cast iron or galvanized steel pipes. While durable, they can become rusted and break. Copper lines also are popular for being heat and corrosion resistant. However, over time, pipe walls can become thin or break if bent in sharp angles.

Modern plumbing techniques involve PVC or PEX water lines, depending on how the lines will be used.

Ensuring your plumbing systems are updated reduces the risk of a surprise water line break, which can create a loss well into the thousands. Again, it is important to consult with a licensed and insured plumber for inspection and updating as needed.

Other updates that homeowners can do may not affect insurance premiums but can be important in the event of a loss. Replacing windows, updating flooring, and changing or updating heating/cooling systems can change a home’s replacement or rebuild value, which is what most home insurance companies rely on in the event of a total-loss claim.

As with any insurance issue, it is important to meet and review policies with a licensed agent.

Alan T. Girton is a veteran agent with Indiana Farm Bureau Insurance. To learn more, visit https://www.infarmbureau.com/agents/Alan-Girton-Howard-Kokomo-IN

| A guest post by

|